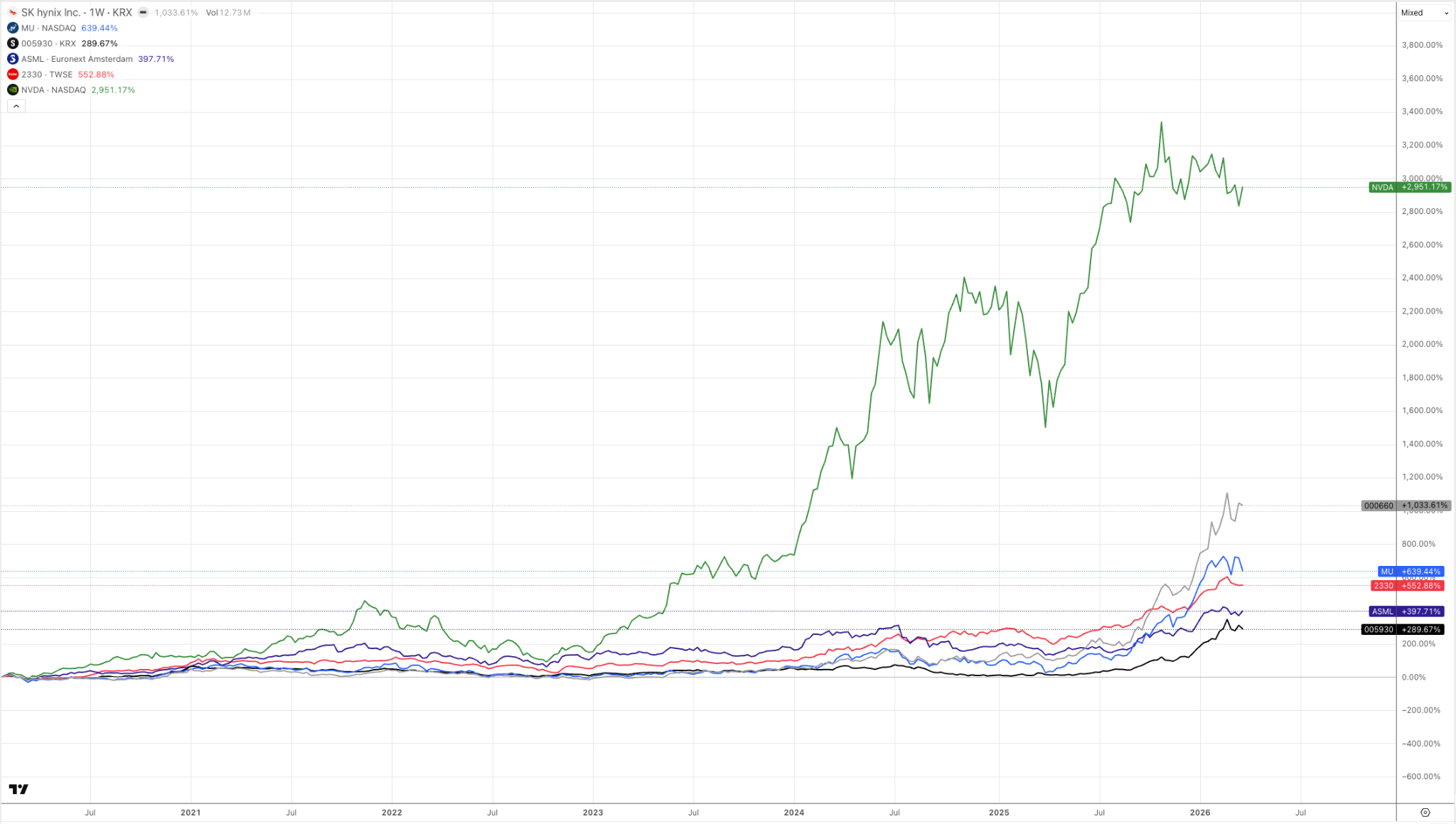

SK hynix Bets on AI Memory Boom with $67B Investment Push

The memory segment is a key driver of transformation within the semiconductor industry and is being propelled by capital expenditure as a result of the continued artificial intelligence (AI) boom. SK Hynix, which is planning to issue depositary receipts in American markets, is using this upcoming IPO to fund a significant investment programme of approximately 67 billion dollars. As part of this, the company plans to allocate up to 10 billion dollars in additional capital to position itself as a leader in high-performance memory, which is a major source of demand for AI infrastructure.

As competitors such as Micron Technology and Samsung Electronics are also investing tens of billions of dollars in the memory segment, this signals the beginning of a new investment cycle in which the scale of capital becomes a key factor in determining competitiveness within the semiconductor industry.

The technological demands of this cycle have increased the financial burden on participants in the memory market. For example, SK Hynix’s nearly 8 billion dollar contract with ASML for next-generation extreme ultraviolet (EUV) lithography equipment illustrates the shift of memory manufacturing towards more advanced processes, which were previously associated mainly with logic chips. The growth of high bandwidth memory (HBM) and the development of multi-chip architectures will require tighter integration between logic and memory, as well as greater reliance on specialised suppliers such as TSMC. As a result, memory manufacturers will need not only to scale investment but also to pursue greater technological independence within their operations, often through vertical integration strategies similar to those seen at Samsung Electronics.

The reasons for making these investments based on financial rationale are becoming clearer in the context of today’s market dynamics: the DRAM sector's revenue almost tripled in terms of dollar value between 2020 and 2025, increasing from $50 billion to approximately $150 billion, with corresponding annual growth rates exceeding 50% and making memory one of the largest beneficiaries of the upcoming AI funding boom; in addition to this trend, Micron Technology has demonstrated the strongest overall growth momentum relative to all the other large players in 2020–2025 by increasing its revenue by greater than 50%, further solidifying its place on the heatmap, while Nvidia continued to lead in absolute dollar amounts; and lastly, market share concentration is becoming increasingly high, whereby several major companies are expanding their market shares at a much faster rate than their competitors, which will likely lead to further industry consolidation and increase barriers to entry for potential new competitors.

More focus is placed on matching investment cycle timing to actual demand developments. Memory market revenue growth mainly comes from the rise in price, not from the rise in volume. This suggests that the memory market may be vulnerable to a market correction, given that large companies are growing their capital expenditures, leading to excess supply in the next few years. A slowdown in worldwide AI infrastructure growth is also likely to lead to an increase in companies’ dependence on external financing (i.e., public capital markets) for their capital expenditures due to the increased risk of the cycles and possible overheating of the market caused by the combination of significantly increased capital expenditures, significant reliance on limited supplies of technology, and a high degree of concentration of market share.

Investment trends in the semiconductor industry are beginning to shift as a result of these changing dynamics. Demand for memory products (principally based on AI) continues to drive revenue growth as well as large investments in manufacturing and technological development. However, the combined effects of increased capital expenditures, significant reliance on a limited technology supply chain, and increased levels of market share concentration mean that this will lead to a much higher level of cycle risk and potential overheating going forward. Therefore, for investors, this represents a transition from a phase of extremely fast growth to a phase of more balanced valuation based on how effectively companies can align their investments to actual demand and operate efficiently in a more competitive and expensive technology environment.